-

-

AppealedTwo years later, Google appeals antitrust ruling for search: cites 'hard work' for top spot

AppealedTwo years later, Google appeals antitrust ruling for search: cites 'hard work' for top spot -

Protecting privacyI protect my privacy while using Meta smart glasses with these 3 settings — and you can too

Protecting privacyI protect my privacy while using Meta smart glasses with these 3 settings — and you can too -

AI backlash growsFormer Google CEO Eric Schmidt booed after AI remarks at the University of Arizona2 Comments

AI backlash growsFormer Google CEO Eric Schmidt booed after AI remarks at the University of Arizona2 Comments -

Ecosystem handoffAndroid 17 catches up to Apple with a long-overdue cross-device upgrade

Ecosystem handoffAndroid 17 catches up to Apple with a long-overdue cross-device upgrade -

HardwiredIt's getting harder to ignore Gemini in Google services, and that's a problem

HardwiredIt's getting harder to ignore Gemini in Google services, and that's a problem -

Quiet downgradeThe Google AI Pro plan just got a quiet downgrade, here is the new deal2 Comments

Quiet downgradeThe Google AI Pro plan just got a quiet downgrade, here is the new deal2 Comments -

Another chunk... goneMeta chops 8,000 in May layoff spree, and it's only getting worse

Another chunk... goneMeta chops 8,000 in May layoff spree, and it's only getting worse

-

-

-

AI backlash growsFormer Google CEO Eric Schmidt booed after AI remarks at the University of Arizona2 Comments

-

Quiet downgradeThe Google AI Pro plan just got a quiet downgrade, here is the new deal2 Comments

-

Gemini takeover5 important Gemini updates from Google I/O that could genuinely save you time

Gemini takeover5 important Gemini updates from Google I/O that could genuinely save you time -

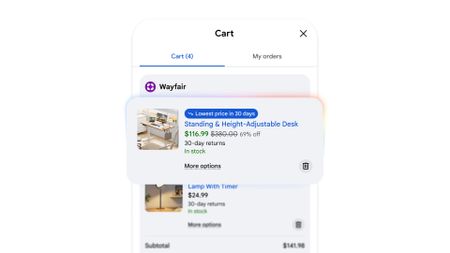

AI x online shoppingForget CamelCamelCamel: Google's new Universal Cart will track prices and find deals for you

AI x online shoppingForget CamelCamelCamel: Google's new Universal Cart will track prices and find deals for you -

Genie "magic"Dreaming of Project Genie? Google I/O unveils 'Street View,' putting imaginary worlds into ours

Genie "magic"Dreaming of Project Genie? Google I/O unveils 'Street View,' putting imaginary worlds into ours -

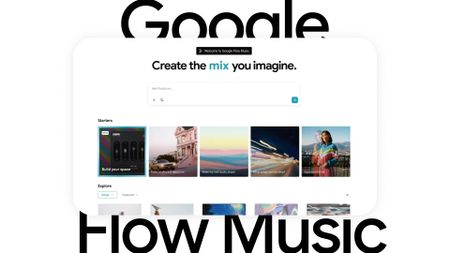

AI crazyGoogle I/O gets into a Flow: preps Flow Music app and generative editing for on-the-go

AI crazyGoogle I/O gets into a Flow: preps Flow Music app and generative editing for on-the-go -

Let AI handle itGoogle's new Gemini features will take all the annoying busywork off your plate

Let AI handle itGoogle's new Gemini features will take all the annoying busywork off your plate -

Assistant rebootPlanning a wedding? Google's new Gemini Spark AI agents might actually help

Assistant rebootPlanning a wedding? Google's new Gemini Spark AI agents might actually help -

Gemini goes furtherNot just an OS: Gemini Intelligence shines with Android automation this summer

Gemini goes furtherNot just an OS: Gemini Intelligence shines with Android automation this summer

-

-

-

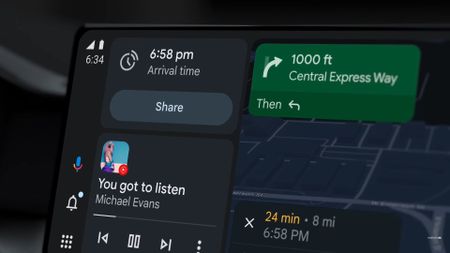

Take a driveAndroid Auto gets a fresh take on Google Maps navigation, teases more Gemini at the Android Show

Take a driveAndroid Auto gets a fresh take on Google Maps navigation, teases more Gemini at the Android Show -

Smarter driving5 Android Auto settings I always change on any new Android phone

Smarter driving5 Android Auto settings I always change on any new Android phone -

Android Auto bug is making the signal icon vanish for some users

Android Auto bug is making the signal icon vanish for some users -

Finally fixedAndroid's Driving Mode is finally smarter about when it turns on3 Comments

Finally fixedAndroid's Driving Mode is finally smarter about when it turns on3 Comments -

Where'd it go?Something's missing: Android Auto users report a jarring bug in Google Maps

Where'd it go?Something's missing: Android Auto users report a jarring bug in Google Maps -

It might finally happenAndroid Auto may finally let you cast media from your phone

-

Gemini-fiedGemini transforms Android Auto with new AI features for a smarter drive

-

Bye, Assistant!Gemini for Android Auto is starting to replace Google Assistant

Bye, Assistant!Gemini for Android Auto is starting to replace Google Assistant -

Eyes on the RoadGoogle starts quietly rolling out an essential button on Android Auto

Eyes on the RoadGoogle starts quietly rolling out an essential button on Android Auto

-

-

-

Ecosystem handoffAndroid 17 catches up to Apple with a long-overdue cross-device upgrade

-

Visuals take center stageAndroid 17 QPR1 Beta 3 is here, and it’s all about the boring fixes you actually wanted

Visuals take center stageAndroid 17 QPR1 Beta 3 is here, and it’s all about the boring fixes you actually wanted -

Emojis leakHere's your first look at more of Google's new 3D emojis for Android 17

Emojis leakHere's your first look at more of Google's new 3D emojis for Android 17 -

Sharing gets easierQuick Share is getting a useful upgrade for sharing files with iPhones

Sharing gets easierQuick Share is getting a useful upgrade for sharing files with iPhones -

What's nextAndroid 17: Everything you need to know2 Comments

What's nextAndroid 17: Everything you need to know2 Comments -

Big Android reveals5 huge Android 17 upgrades are coming this year — Here are the best new features announced at The Android Show

Big Android reveals5 huge Android 17 upgrades are coming this year — Here are the best new features announced at The Android Show -

Stay safeYour Android security and privacy got huge upgrades—The Android Show reveals all

Stay safeYour Android security and privacy got huge upgrades—The Android Show reveals all -

Magic PointerI didn't think the desktop cursor needed reinventing — Googlebooks are proving me wrong6 Comments

Magic PointerI didn't think the desktop cursor needed reinventing — Googlebooks are proving me wrong6 Comments -

Android gets personalAndroid 17 is fixing two things that have annoyed me for years

-

-

-

A fresh coat of paintGoogle's new gradient icons for Gmail, Calendar, Drive and more are finally rolling out

A fresh coat of paintGoogle's new gradient icons for Gmail, Calendar, Drive and more are finally rolling out -

That's a big cutGoogle may be cutting free Gmail storage for new accounts down to 5GB

That's a big cutGoogle may be cutting free Gmail storage for new accounts down to 5GB -

Useful parroting?Gmail's 'Help me write' can now mimic how you speak to create emails for you

Useful parroting?Gmail's 'Help me write' can now mimic how you speak to create emails for you -

New address, same inboxI changed my embarrassing Gmail username without losing anything, and you can too2 Comments

-

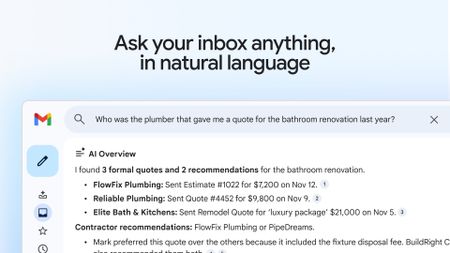

That's a steep priceGmail's new AI Inbox is here, but it'll cost you $250 a month

That's a steep priceGmail's new AI Inbox is here, but it'll cost you $250 a month -

Gemini takes overGmail is getting a new AI inbox as Google brings Gemini front and center2 Comments

Gemini takes overGmail is getting a new AI inbox as Google brings Gemini front and center2 Comments -

A long-awaited featureGmail might finally let you switch to a new address without starting over

-

Get a previewGmail gives Android users a window into email attachments with this update

-

Sleigh Bells ring...Google brings a unified 'Purchases' tab to Gmail ahead of the holiday rush

-

-

-

Bye, AssistantGoogle Assistant could shut down for Android Auto in March 2026

Bye, AssistantGoogle Assistant could shut down for Android Auto in March 2026 -

New look!Google's song search evolves with a modern Gemini-inspired UI on Android

New look!Google's song search evolves with a modern Gemini-inspired UI on Android -

New look!Google's voice and song search gets a major overhaul on Android after years

New look!Google's voice and song search gets a major overhaul on Android after years -

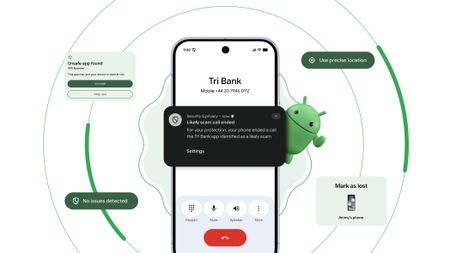

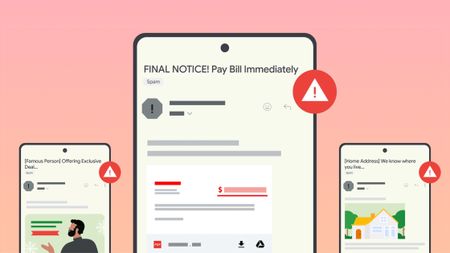

Stay in the knowGoogle introduces new tools to help users fight against evolving phishing scams effectively

Stay in the knowGoogle introduces new tools to help users fight against evolving phishing scams effectively -

Google OutageGoogle, Gmail, and Meet hit by widespread outage, causing login issues

Google OutageGoogle, Gmail, and Meet hit by widespread outage, causing login issues -

New voicesGoogle is spicing up its voice list on Search, according to a new leak

New voicesGoogle is spicing up its voice list on Search, according to a new leak -

New Google AI plansNew Google AI Pro and $249/month Ultra subscription announced at I/O

New Google AI plansNew Google AI Pro and $249/month Ultra subscription announced at I/O -

Easy-peesyGoogle app on iOS gets a new feature that will 'Simplify' text online

-

ByeGoogle officially killed Driving Mode after stripping most of its features in 2024

ByeGoogle officially killed Driving Mode after stripping most of its features in 2024

-

-

-

Don't stressGet in: Android Auto EVs see AI battery predictions in Google Maps for stress-free plans

-

It's just like new'Immersive Navigation' in Google Maps is like opening a new app for the modern era of driving

It's just like new'Immersive Navigation' in Google Maps is like opening a new app for the modern era of driving -

Limiting features?Google Maps might keep things from you if you don't sign in to an account

-

Test runGoogle Maps might get a trial space for new features, and 'Ask Maps' could headline

Test runGoogle Maps might get a trial space for new features, and 'Ask Maps' could headline -

Out on a walkMy walks just got a lot better, as Google says 'Gemini in Navigation' supports more

Out on a walkMy walks just got a lot better, as Google says 'Gemini in Navigation' supports more -

Better battery lifeHow to enable and use Google Maps power saving mode

Better battery lifeHow to enable and use Google Maps power saving mode -

Let's go thereGoogle Maps gets a major upgrade with Gemini for smooth navigation on Android and iOS

-

Let's go thereGoogle Maps gets a Gemini boost to help you navigate the roads like a pro

-

Double RainbowHere's what the redesigned Google Photos and Maps icons look like

Double RainbowHere's what the redesigned Google Photos and Maps icons look like

-

-

-

How ToThis is the best Google Pay feature you're not using in India

How ToThis is the best Google Pay feature you're not using in India -

How ToI used this hidden Google Pay feature to automate credit card bill payments

How ToI used this hidden Google Pay feature to automate credit card bill payments -

No more drainAndroid’s next update is finally addressing your phone’s biggest battery hogs

No more drainAndroid’s next update is finally addressing your phone’s biggest battery hogs -

On TimeGoogle Wallet is helping Android users effortlessly catch their plane or train

On TimeGoogle Wallet is helping Android users effortlessly catch their plane or train -

Quick TapsGoogle Pay's fresh updates will unlock better shopping rewards for Chrome users

Quick TapsGoogle Pay's fresh updates will unlock better shopping rewards for Chrome users -

Pay Your WayAndroid users get another option to pay later with Klarna on Google Pay

Pay Your WayAndroid users get another option to pay later with Klarna on Google Pay -

Easier accessGoogle Wallet brings digital ID support to UK, more US states

Easier accessGoogle Wallet brings digital ID support to UK, more US states -

Now arriving at...Google Wallet brings real-time train status alerts to Android, and teases I/O 2025

-

Next stop is...Londoners can join the Google Pay 'Tube Challenge' for badges and city lore

Next stop is...Londoners can join the Google Pay 'Tube Challenge' for badges and city lore

-

-

-

Play gets smarterGoogle Play is getting a huge AI upgrade with Ask Play and Play Shorts

Play gets smarterGoogle Play is getting a huge AI upgrade with Ask Play and Play Shorts -

Create appsThis Google AI tool can now build Android apps from text prompts

Create appsThis Google AI tool can now build Android apps from text prompts -

It's a problemGoogle puts apps that'll drain your battery on blast in updated Play Store listings

It's a problemGoogle puts apps that'll drain your battery on blast in updated Play Store listings -

A downgrade to downgradingGoogle just made uninstalling system app updates more complicated

-

Free cashHere's when Google Play Store users will get an automatic cash settlement payout3 Comments

-

You win!Focus Friend and Pokémon TCG Pocket shine in Google Play's Best of 2025 awards

You win!Focus Friend and Pokémon TCG Pocket shine in Google Play's Best of 2025 awards -

Find it fasterGoogle Play enhances search with new 'Where to watch' streaming feature

-

No more siftingGoogle's upcoming review search feature might soon help you save time on the Play Store

No more siftingGoogle's upcoming review search feature might soon help you save time on the Play Store -

Gift cards go greenYou can now send Starbucks and Disney gift cards straight from Google Play

Gift cards go greenYou can now send Starbucks and Disney gift cards straight from Google Play

-

-

-

Protecting privacyI protect my privacy while using Meta smart glasses with these 3 settings — and you can too

-

Another chunk... goneMeta chops 8,000 in May layoff spree, and it's only getting worse

-

AI everywhereMeta's Muse Spark arrives on AI Glasses Gen 1, Ray-Ban Display waits for now

AI everywhereMeta's Muse Spark arrives on AI Glasses Gen 1, Ray-Ban Display waits for now -

AI, VR, AI, VRMeta Connect 2026 confirmed for September, and we're thinking AI and Quest

AI, VR, AI, VRMeta Connect 2026 confirmed for September, and we're thinking AI and Quest -

Per your requestMeta's AI plans look agentic with a potential Instagram bot that shops for you

Per your requestMeta's AI plans look agentic with a potential Instagram bot that shops for you -

Encryption is goneMeta can see your Instagram messages now, and it's time to stop using it

Encryption is goneMeta can see your Instagram messages now, and it's time to stop using it -

AI AI AI AI AI AI AIMeta's Q1 2026 earnings are in, and it looks like Zuckerberg's blank check for AI spending is raising some eyebrows

AI AI AI AI AI AI AIMeta's Q1 2026 earnings are in, and it looks like Zuckerberg's blank check for AI spending is raising some eyebrows -

new oversightMeta gives parents a way to see what their teens are asking its AI

new oversightMeta gives parents a way to see what their teens are asking its AI -

Three-point beast?Meta's Threads is going live with chats for big moments, like the NBA Finals

Three-point beast?Meta's Threads is going live with chats for big moments, like the NBA Finals

-

-

-

Spotify drives engagement the right way, expands into 'Fitness' with Peloton

Spotify drives engagement the right way, expands into 'Fitness' with Peloton -

A worthy upgradeSpotify looks brand new on tablets with a design rework that makes total sense

A worthy upgradeSpotify looks brand new on tablets with a design rework that makes total sense -

Reading is goodSpotify, Bookshop expand to US, and 'Page Match' gets huge language support

Reading is goodSpotify, Bookshop expand to US, and 'Page Match' gets huge language support -

Podcasts this timePodcasts meet Spotify's Prompted Playlists for curious Premium US beta testers

Podcasts this timePodcasts meet Spotify's Prompted Playlists for curious Premium US beta testers -

A vast webIt's in the SongDNA: an 'immersive' Spotify test that lets you discover everyone involved

A vast webIt's in the SongDNA: an 'immersive' Spotify test that lets you discover everyone involved -

Your tasteAll to your liking: Spotify's 'Taste Profile' beta puts you in charge of the music you find

Your tasteAll to your liking: Spotify's 'Taste Profile' beta puts you in charge of the music you find -

InspiredSpotify's 'About the Song' beta lets you into the stories behind the artist's creation

InspiredSpotify's 'About the Song' beta lets you into the stories behind the artist's creation -

Turn the pageI'll never stop reading with Spotify, Bookshop's partnership and 'Page Match' on Android

Turn the pageI'll never stop reading with Spotify, Bookshop's partnership and 'Page Match' on Android -

I can show you the...This Spotify update lets us take our lyrics offline, and there's more for users globally

I can show you the...This Spotify update lets us take our lyrics offline, and there's more for users globally

-

-

-

X is down againX faces major outage as 78K users report disruption this morning

X is down againX faces major outage as 78K users report disruption this morning -

Where are you?X's new 'transparent' location labels for accounts have people questioning everything

-

Partial outageFacing trouble logging into X? You're not alone — here’s the scoop!

Partial outageFacing trouble logging into X? You're not alone — here’s the scoop! -

Twitter is downIt wasn't just you — X (Twitter) resolved a major outage today

Twitter is downIt wasn't just you — X (Twitter) resolved a major outage today -

Whistleblower calls out Twitter for spambots and mishandling user data

Whistleblower calls out Twitter for spambots and mishandling user data -

What is free speech?

What is free speech? -

Twitter makes it easier to search for Communities on the web

Twitter makes it easier to search for Communities on the web -

Massive Twitter outage ends after about 90 minutes

Massive Twitter outage ends after about 90 minutes -

House committee summons Meta, Alphabet, Twitter and Reddit over Capitol riot

House committee summons Meta, Alphabet, Twitter and Reddit over Capitol riot

-

-

-

Wear OS updateWear OS 7 officially revealed: Here are the biggest new features

Wear OS updateWear OS 7 officially revealed: Here are the biggest new features -

About timeGoogle just announced Wear OS 6.1, and it adds a time zone feature I've wanted for years

About timeGoogle just announced Wear OS 6.1, and it adds a time zone feature I've wanted for years -

A proper upgradeSpotify on Wear OS just got a big redesign that makes it much easier to use

A proper upgradeSpotify on Wear OS just got a big redesign that makes it much easier to use -

Standalone protectionWear OS can now send life-saving earthquake alerts without your phone

Standalone protectionWear OS can now send life-saving earthquake alerts without your phone -

Wear thisThe best Wear OS watch

Wear thisThe best Wear OS watch -

Visual messA major Wear OS 6 bug is ruining custom watch faces on Pixel and Galaxy Watches

Visual messA major Wear OS 6 bug is ruining custom watch faces on Pixel and Galaxy Watches -

Wearables WeeklyWhat I expect and want to see from Android smartwatches in 2026

Wearables WeeklyWhat I expect and want to see from Android smartwatches in 2026 -

Wearables WeeklyWear OS in 2025: How Pixel, Galaxy, and OnePlus smartwatches fared against our expectations2 Comments

Wearables WeeklyWear OS in 2025: How Pixel, Galaxy, and OnePlus smartwatches fared against our expectations2 Comments -

You're green!Androidify for Wear OS: turn yourself into an Android bot for your Pixel Watch

You're green!Androidify for Wear OS: turn yourself into an Android bot for your Pixel Watch

-

-

-

More AI slopGoogle's new YouTube AI tools could make AI slop impossible to escape

More AI slopGoogle's new YouTube AI tools could make AI slop impossible to escape -

The Premium pressureYouTube on mobile makes livestream ads way less annoying, but there's a caveat

The Premium pressureYouTube on mobile makes livestream ads way less annoying, but there's a caveat -

Half off YouTubeYou can now get YouTube Premium for half price with Google AI Pro

Half off YouTubeYou can now get YouTube Premium for half price with Google AI Pro -

Shorts, gone (almost)YouTube now lets you turn off Shorts

Shorts, gone (almost)YouTube now lets you turn off Shorts -

Premium gets pricierYouTube Premium just got a price hike, and it's not a small one3 Comments

Premium gets pricierYouTube Premium just got a price hike, and it's not a small one3 Comments -

Trying something newYouTube tests a couple of speedy, 'on-the-go' features for busy Android viewers

-

Sort of supportedYouTube now works with Android Auto, but not in the way you'd expect

Sort of supportedYouTube now works with Android Auto, but not in the way you'd expect -

Check it outDiscovering YouTube videos with 'Previews' is a change it wants to see if you like

Check it outDiscovering YouTube videos with 'Previews' is a change it wants to see if you like -

Take this, but make it thisA twist like no other: YouTube Shorts lets you 'Reimagine' with Gemini and Veo

Take this, but make it thisA twist like no other: YouTube Shorts lets you 'Reimagine' with Gemini and Veo

-